There’s a moment late in the homebuying process that catches a lot of people off guard. It’s when they realize closing costs are not the same as cash to close.

It usually happens after the inspections. After the appraisal. After the loan gets cleared to close. After the buyer has emotionally moved into the house in their head.

The borrower asks a simple question: “So… how much do I need to bring to closing?”

And the number is higher than expected. Sometimes much higher.

Not because anyone lied or because something went wrong. It’s just because the borrower never had a clear picture of cash to close in the first place.

This is where a lot of otherwise smart, prepared buyers get burned; both financially and emotionally.

It’s not their fault. Failing to prep the borrower falls on the loan officer’s shoulders.

The Stories Buyers Don’t Expect to Be Part Of

I’ve seen versions of this play out over and over:

A buyer plans for their down payment, but doesn’t realize closing costs are a whole different bucket of expenses

None of these buyers were reckless. Most were thoughtful, detail-oriented people.

The issue wasn’t the borrower being dumb or irresponsible. The problem was vagueness on the part of the loan officer. And I’ll admit, I was guilty of this more than once in the beginning of my career.

When the only guidance is a rough estimate and a shrug of “we’ll know more later,” the stress doesn’t disappear, it just gets deferred to the worst possible moment.

Unfortunately, I hear countless stories of seasoned loan officers that still operate with this type of vagueness. There is no reason to put up with it when a little time and attention is all it takes to help avoid a last-minute stress bomb.

And just for a little glimmer of hope in case you do have a bad loan officer that doesn’t prep you: It is not likely that the cash-to-close amount would be so high that you can’t come up with the money and the deal will fall through. The reason for this is that part of what underwriting looks at is whether you have proof of enough assets to bring the appropriate cash-to-close to the closing table. Honestly, this is what bad loan officers rely on – so long as the funds exist somewhere, they don’t care what pain or shock everyone has to suffer to actually get the money to title at closing.

But, I’d recommend working with a loan officer that will take the time to clearly explain cash to close ahead of time.

Why Vague Estimates Create Late-Stage Anxiety

Early in the process, cash to close is often presented as a range. That’s normal. Some costs do change.

But too often, that range is:

- Too wide to be useful

- Too abstract to emotionally prepare for

- Too disconnected from the buyer’s actual bank account

So buyers anchor on the lowest number they hear. That’s human nature.

Then, weeks later, when the real numbers firm up, it feels like a surprise, even if it “technically” isn’t.

This is one of the quiet themes I unpacked more deeply in this month’s Substack: Most buyer stress isn’t caused by the cost itself. It’s caused by when and how clarity shows up. The worst pain of all isn’t even when pain shows up at the closing table: it’s when the budget gets squeezed months or years later as a result of a loan that’s too expensive.

What Changes When You Plan for Cash to Close Early

When buyers take the time to map out cash to close before they’re under contract, something subtle but important shifts.

They stop asking:

“Can I afford this house?”

And start asking:

“Am I comfortable with how this will feel when the money actually moves?”

That’s a very different question.

Early planning allows buyers to:

- Separate must-have cash from buffer cash

- See which costs are fixed vs. variable

- Decide ahead of time what feels tight vs. manageable

By the time closing day comes around, the number may not be exactly what they planned for at the beginning, but it will be closer and familiar – not a bombshell they never saw coming.

And that familiarity is what reduces panic.

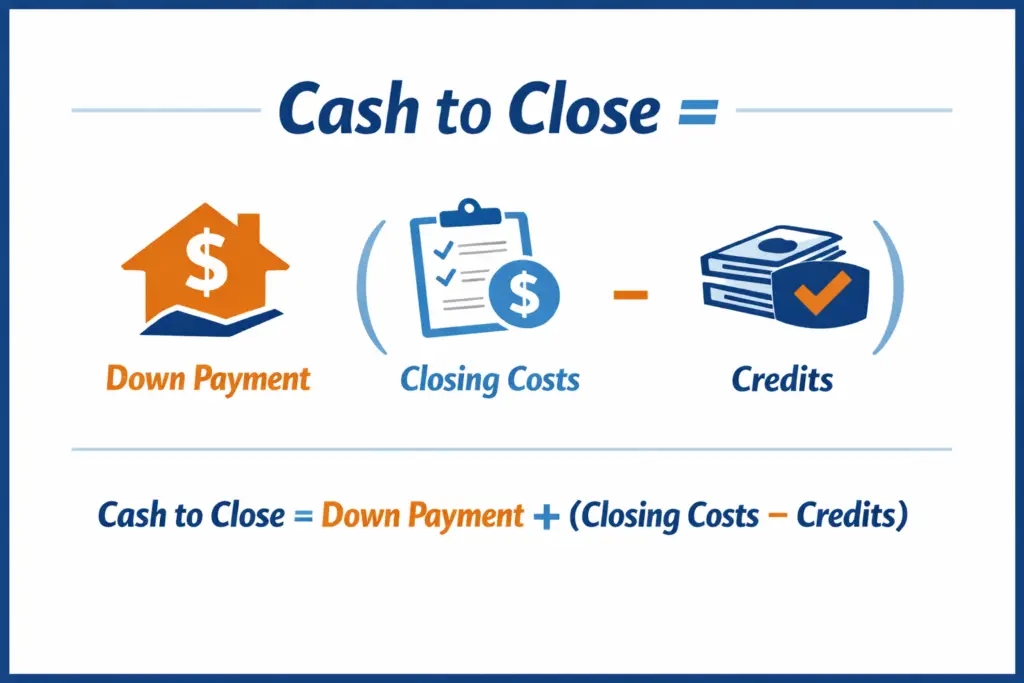

Cash to Close Isn’t Just a Math Problem

On paper, cash to close is straightforward:

Cash to Close = Down Payment + (Closing Costs – Earnest Money – Seller Credits)

But emotionally, it’s loaded.

This is often the largest single transfer of money a buyer has ever made. When the number shows up late and feels bigger than expected, it can trigger doubt, regret, and second-guessing, and even a sense of betrayal, right when buyers should be feeling settled, confident and supported.

In my mind, the goal with cash to close isn’t to eliminate uncertainty. It’s to contain it early, when it’s easier to process.

That’s why I often encourage buyers to treat cash to close as a planning exercise, not a final figure.

A More Grounded Way to Approach It

If you want to avoid the late-stage shock, here’s the mindset shift:

Don’t ask for the number. Ask for the components.

When you understand what makes up cash to close, and which parts are likely to move, you regain control over the experience.

This is also where tools help. A simple cash-to-close worksheet forces the conversation earlier, when there’s still room to adjust expectations, timelines, or even the target price range. (You can download my cash-to-close worksheet here: https://davethemortgageguy.loans/cash-to-close-estimator/)

And when paired with a broader framework, like the Safe Buying Box I’ve written about elsewhere (you can read it here), it becomes easier to see whether a purchase fits not just your budget, but your nervous system.

The Takeaway

Most buyers don’t get burned because they can’t afford the house. They get burned because clarity arrives too late.

Cash to close is where that shows up most often.

Plan for it early. Break it down. Make the uncertainty visible before you’re emotionally committed.

If you want to go deeper on the thinking behind this, this month’s Substack expands on how early financial clarity changes the entire buying experience, not just the numbers.

And if you want something practical to work through, the cash-to-close worksheet and Safe Buying Box are designed to support exactly this stage of planning, without adding pressure or urgency.

Clarity doesn’t remove the cost, but it does remove the shock.

If you want to learn a little more about cash to close, as well as the three other numbers that factor into buying a home, check out my video below: